Back in January, Christopher Leonard warned in Business Insider “the Fed is popping the ‘everything bubble’ — and catapulting the stock market into chaos.” Leonard notes that despite price inflation rising at the fastest pace in 40 years and a certifiably uneven recovery from the recession of 2020, Federal Reserve Chairman Jerome Powell remains confident that the Fed is on top of it. In a sense, Leonard says, Powell is telling the truth, “but what Powell leaves unsaid is that using these tools could create a disaster. And what the Fed chair definitely won’t tell you is that this mess will be all the more catastrophic because of the Fed’s own policies over the past 12 years.”

Leonard notes the massive amount of money injected by the Fed into the economy since 2009:

“Between 1913 and 2008, the Fed used this power to gradually increase the money supply from effectively zero to roughly $900 billion. Then between late 2008 and mid-2014, the Fed created a program called “quantitative easing,” which tried to bolster the economy by injecting 3 trillion new dollars into the system.” That’s three centuries worth of money printing in about five years. During the same period, the Fed launched another unprecedented program — it kept interest rates pegged at zero.”

…When the Fed pumps new money into the banking system through quantitative easing, it does so by buying up long-term Treasuries, which pushes down yields. In turn, investors — from average Americans saving for retirement to complex hedge funds — are forced into what has become known as the “search for yield,” a scramble to earn what they need by putting their money into riskier investments.

Trillions of dollars injected into the system forced investors to chase yield by putting their money in risky assets like shares of unprofitable companies, securitized leveraged loans, and bonds for shady overseas companies. This, in turn, created what Wall Street traders call the “everything bubble.” Usually, asset bubbles pop up in a certain segment of the economy, like housing or high-flying tech stocks, but traders are worried that the search for yield has pushed so many dollars into so many risky assets that the bubbles are everywhere at once.

In order to fight inflation, Powell and his compatriots must raise short-term interest rates — thereby taking some money out of the system. But when interest rates go up, investors can start earning more money in safe havens like the 10-year Treasury and pull back from the risky investments they were incentivized to make over the last decade. And when that happens … bubbles can pop.

…during the Fed’s decadelong experiment, the value of stocks rose steadily in spite of weak economic growth — the Dow Jones Industrial Average skyrocketed 77% between 2010 and 2016. One typically caustic hedge-fund trader described to me the frothy stock market of 2016 as being like the crowded deck of the Titanic as it sank. The deck wasn’t crowded because it was a great place to be; it was crowded because people had nowhere better to go.”

As Leonard points out, the “Everything Bubble” already came close to popping right at the tail end of 2018 and into early 2019. At this time, as the Fed raised rates, “investors had nowhere to hide” and “for the first time in decades, every major type of investment…fared poorly, as the outlook for economic growth and corporate profits is dampened by rising trade tensions and interest rates.” Powell then “pivoted”, deciding to reverse Fed policy in an attempt to postpone the crash.

During the 2018-2019 panic, there were numerous reports in business media about the impending catastrophe. On Dec 10, 2018, the New York Times asked readers if they were “Ready for the financial crisis of 2019?” The Times noted that hedge funds had had their worst year since 2008, household debt had hit a record high of $13.5 trillion (“up $837 billion from the previous peak, which preceded the Great Recession”),and that 20% of the loans which made up the $1.5 trillion in student debt were delinquent or in default.

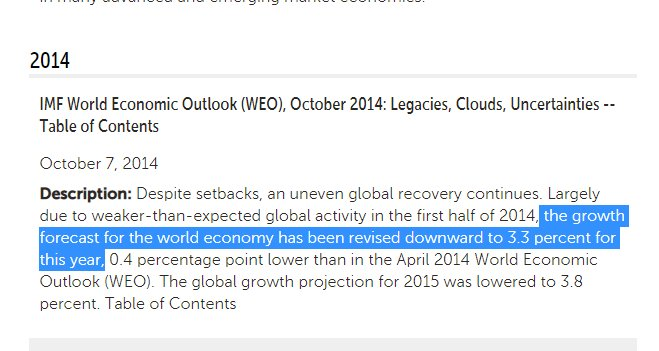

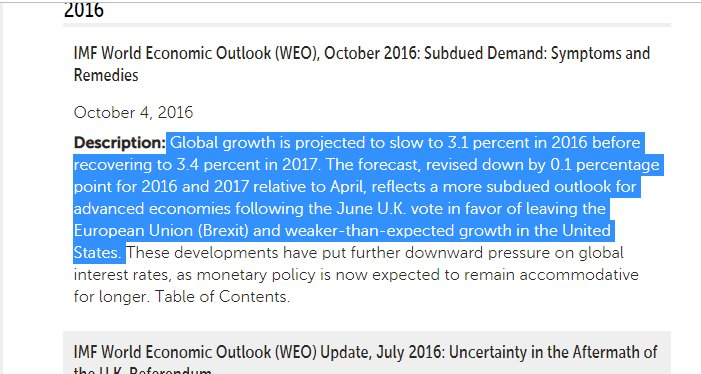

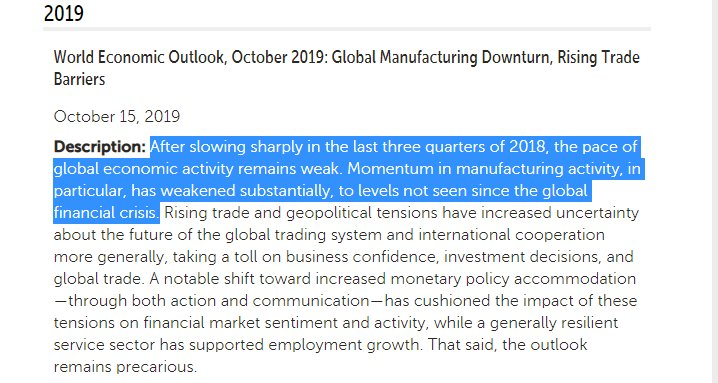

Earlier, in 2015, there were murmurings of a “global economic slowdown”, an anxiety boosted by IMF World Economic Outlook reports which showed a general slowdown in global growth between 2014-2019.

In 2019, massive amounts of corporate debt delivered a negative or “inverted” yield curve, a generally agreed upon sign of market correction and/or financial crash which hadn’t occurred since 2008. “Loans to companies with large amounts of outstanding debt — known as leveraged lending — grew by 20 percent in 2018 to $1.1 trillion…The share of new, large loans going to the comparatively risky borrowers now exceeds peak levels reached previously in 2007 and 2014.”

As Murray Sabin explains in Fortune:

“The yield curve was virtually inverted at the end of 2019, suggesting that a recession would begin sometime in 2020. However, the lockdowns in response to COVID-19 caused an economic downturn in early 2020, not a typical cyclical recession.

Now the economy is in another cyclical upswing because the Federal Reserve injected $4 trillion of liquidity to “simulate” the economy. At the most recent meeting of the Federal Open Market Committee (FOMC), it was decided to reduce monthly purchases from $120 billion to $105 billion. In other words, the Fed will continue to have its foot on the monetary pedal even as the inflation rate recently topped 6% year over year. In the past accelerating inflation would set off alarm bells at the Fed to raise interest rates to dampen inflationary pressure and expectations. Currently, the thinking at the Fed is that price inflation is “transitory” and therefore monetary policy does not have to be tightened.”

In November, 2021, Michael O’Rourke, chief market strategist at JonesTrading, pointed out that “…the S&P 500’s market capitalization is 177% of U.S. GDP. During the 2000 tech bubble, the S&P 500’s market capitalization peaked at 121% of nominal gross domestic product…” O’Rourke points to the “painful” 80% decline for the Nasdaq Composite between March 2000 and October 2002. “The broad tape is 50% more expensive today than March 2000.” That same month MarketWatch reported Morgan Stanely’s concern that, “The Federal Reserve’s easy monetary policy and the spike in the pace of inflation have left investors with negative real interest rates, which are fuel for asset bubbles.” Lisa Shalett, CIO of Morgan Stanley Wealth Management, wrote that the difference between the fed-funds rate and the consumer-price index, which measures inflation, “is widest in the 60-year history of the inflation gauge.”

Despite these trends, the massive stock-market gains of the mid-2010s extended into 2020, even during the initial COVID restrictions. The Dow Jones has skyrocketed 26% since the end of 2019. In October, 2021, James Gorman, CEO of Morgan Stanely, begged the Fed to “prick this bubble a little bit.” According to Gorman, “Money is a bit too free and available right now.” John Waldron, President of Goldman Sachs Group Inc. and Larry Fink, CEO of BlackRock, both concur with Gorman, with Fink saying inflation is “definitely not transitory.” Jamie Dimon, the head of JPMorgan Chase, has said inflation will likely not ease anytime soon.

However, as Leonard notes, these pleas were ignored:

“Investors, desperate for gains, have eschewed the stocks of safe companies with strong profits and instead pumped their money into companies telling pie-in-the-sky stories about their future — and their future stock gains. The market value of Tesla, for example, rose nearly $200 billion in December, according to The Wall Street Journal, which was more than the total combined value of Ford and General Motors.”

Theranos Was Just the Beginning

As Linette Lopez recently wrote:

“A side effect of making money easy to borrow was that all kinds of garbage ideas could get funding and all kinds of garbage companies could stay in business. Combine that with lax corporate law enforcement and you have Wall Street without consequences. Investors were champing at the bit to pile into companies that used fantastical metrics, like WeWork, and lapped up every utterance from billionaire CEOs who promised flashy technology but consistently under-delivered, like, say, Elon Musk.”

And that was before millions of bored, homebound Americans jumped into the market via Robinhood and other trading apps. Armed with their pandemic-era stimulus checks, they bought crypto, piled into blank-check companies called SPACs, and joined message boards claiming that stocks like AMC and GameStop were going “to the moon.” Awash with capital, companies — especially in tech — saw their valuations leave Earth’s atmosphere and make a home somewhere on Saturn. Short sellers were culled. Value investors went into hiding.”

Lopez’s first point, the massive investment into riskier and shadier businesses that were really good at branding themselves industry disruptors capable of cornering their respective markets at break-neck speed, is exemplified by the now notorious story of Theranos.

As Gavin Benke writes in The Washington Post:

“The political firestorm that broke out surrounding Enron is over — but the corporate practices that drove it are still happening. For example, Elizabeth Holmes, formerly heralded as a Silicon Valley wunderkind for founding and leading the health-care tech company Theranos (and herself the daughter of an Enron executive), is currently on trial for an alleged act of corporate fraud akin to the years-long practice of cooking the books and inflating profits at Enron. And Frances Haugen, a former Facebook employee turned whistleblower, recently testified before Congress to reveal a range of troubling practices at the company.

In fact, the same business culture that allowed Enron to commit fraud for years has also produced companies like Theranos’s and Facebook. All three of these companies are products of a business-oriented fixation on newness, disruption and innovation that took hold during the first dot-com boom in the late 1990s.”

This boom came at the conclusion of a decade-long reverence for “innovation” which was “echoed and amplified” by “business reporters and management consultants” throughout the 1990s. “Later in the decade, Clay Christensen’s book, The Innovator’s Dilemma, introduced terms such as “disruption” into our broader lexicon.”

Gary Hamel, author of the management book Leading the Revolution, used Enron as a primary example of a firm which was “devoid of tradition” and did business through “radical innovation” and “creating revolutions.” Enron, “even announced plans for a unit called Enron Xcelerator, which would develop new lines of business.”

However, many of Enron’s new businesses flopped hard and the company’s ability to “raise money and report spectacular earnings” was revealed to be predicated on “hiding losses through absurdly complicated arrangements with shell companies created in-house.” By December 2001, Enron declared what was, at the time, the largest bankruptcy in American history.

As the BBC reports, after dropping out of Stanford University, Elizabeth Holmes dedicated herself to, “presenting a vision – a mission as she described it – to revolutionise diagnostics.” Despite experts assuring her that the concept behind what became Theranos was unrealistic, Holmes “projected an unfaltering confidence that the technology would change the world.” Holmes was only 19 when she founded Theranos in 2013. The company claimed it could perform blood tests with miniscule samples of blood at record breaking speed. It also sought the development of wearable patches that would adjust the dosage of a drug into the user’s body according to variables in their bloodwork. At its peak in 2014, Theranos was valued at $10 billion after having raised $700 million from venture capitalists and private investors.

In 2015, Theranos was named the 2015 Bioscience Company of the Year by the Arizona BioIndustry Association (AzBio). Just a year earlier, at age 30 and with a net worth of $4.5 billion, Holmes had been named by Forbes as the “world’s youngest self-made billionaire.” The DeVos wealth dynasty, which gaveTrump his Secretary of Education, invested $100 million into Theranos, doubling their initial investment after Holmes convinced them the technology would be a “game changer for healthcare.” (Ironically, the DeVos family’s initial wealth came from the founding of Amway, a notorious multi-level marketing scam) Other investors included Rupert Murdoch, the Walton Family, and the Cox Family. “Capital BlueCross, a Pennsylvania insurer with 725,000 customers, chose Theranos as its preferred lab work provider.”

That same year, Theranos was exposed as having no peer reviewed research published in any major American journal of medicine and as exaggerating a number of the claims about their technology. The Wall Street Journal’s John Carreyou reported that rather than proprietary technology, Theranos was simply using traditional blood testing machines to analyze customer samples. Walgreens and Safeway both ditched major deals with Theranos to set up blood testing centers in their stores using the company’s technology. Arizona’s Department of Health Services reported that Theranos’s Scottsdale lab didn’t measure up to regulations. By 2016, the Securities and Exchange Commission got involved, and two years later the company folded altogether.

Much work was done in the media to portray Holmes as some uniquely evil tech CEO, as someone who was everything wrong with Silicon Valley and the “innovator” and “disruptor” dogmatism that has slowly but surely made its way into every facet of the domestic US economy since the dot-com bubble. Instead, what Holmes represents is the very essence of this dogmatism as such. All one has to do to understand this is parse the dynamics behind Lopez’s second point regarding the GameStop gambit and other bizarre pump n dumps and pyramid schemes which the US public became increasingly involved with during COVID, but which have been an imperative part of economic “digitalization” for years.

An Entire Economy of Pyramid Schemes

For instance, the current poster child for these types of schemes, cryptocurrency, has quite literally always been One Big Scam. As David Golumbia puts it in a fantastic essay, “Cryptocurrency and blockchain projects are so full of frauds and scams that in most cases, “frauds and scams” is a reasonable substitute term to use for them.” Golumbia points out that, while governments at least have to feign regulation of credit union and bank deposits, conflicts of interest, market manipulation and fraud, there is nothing to protect against any of these things in crypto (despite evangelists saying otherwise). “Further,” Golumbia writes, “the much-touted “immutability” of blockchain transactions–the fact that they cannot be changed once completed–means that fraudulent transactions, like ordinary losses, instantly become permanent.”

But don’t just take Golumbia’s word for it; in 2019, at the same time the larger economy nearly crashed for the third time this century, cryptocurrency was ranked as the 2nd riskiest scam of the year by the Better Business Bureau. Furthermore, there are 1,000s of cryptocurrencies now, and only about 20% of them have any level of real success. As for the others, many of them are used for quickfire pump and dump scams taking advantage of digital network effects.

A study of “virtually every pump and dump during a six month period” in 2018, conducted on Discord & Telegram by researchers at the University of Chicago, showed “high levels of concentration in both exchanges employed for pumps and channels involved in running the pumps.” The study describes “several attributes” that “have yielded a robust pump and dump ecosystem at unprecedented scale.” Among these are:

- New social media/technology: Pump-and-dump schemes have proliferated on a

common public medium: Telegram. Telegram is a cloud-based instant messaging service using Voice over Internet Protocol (VoIP). Users can send messages

and exchange files of any type. Messages can be sent to other users individually or to groups of up to 100,000 members. As of March 2018, Telegram had

200 million active users. Pumps also occurred on Discord, a platform with

similar characteristics to Telegram.

• Low cost: The majority of pumps occur on Telegram channels, which are easy

to form and free to join. Channel members are potential participants in pump

and dump schemes.

• Many cryptocurrencies: The explosion of cryptocurrencies have created myriad opportunities for exploitation. Most are thinly traded, creating favorable

conditions for pumpers.

• Many trading platforms: There has been a proliferation of cryptocurrency

exchanges that enable unregulated trade between coins. Exchanges profit from

the transaction fees resulting from pumps.

• Regulators (so far) have mostly taken a hands-off approach.

Therefore, in a time which has been a boom to Big Tech, we have their platforms enabling a massive squeezing of first time and small time investors by highly concentrated groups of scammers. The Chicago University study reports that, “three channels accounted for roughly 45 percent of all the pumps on Telegram during the period we analyze.” And this isn’t just being done on Telegram and Discord. In July 2020, “there was an odd surge in Dogecoin (DOGE) price because of a TikTok trend. A user named jamezg97 uploaded one of the earliest Dogecoin-pumping TikTok videos, which eventually caused its price to surge.”

At this point, social media influencers pumping and dumping crypto, particularly come and go “shitcoins”, has happened so many times it is almost a meme:

“These schemes target low capitalization cryptocurrencies and digital tokens that can easily be manipulated with low trading volumes,” writes Alex Lielacher. “Instead of boiler rooms, the price pumps are conducted by spreading hype and fake information about a coin on social media.”

“In these instances, the influencer tells their millions of followers that they’re making money off a crypto coin. A fraction of their followers will invest in said coin, expecting to make gains as well. As more followers buy-in and the price spikes, the influencer sells their shares and makes a profit, driving the share price down and thus screwing their followers out of the same return. Though different variations of this scenario can play out depending on how the coin functions (some are more transactional while others function more like pyramid schemes), the result is similar— the influencer walks away with profit they indirectly took from their fans’ own pockets.”

This type of scam has even cropped up on OnlyFans; last year three influencers in Australia were heavily criticized by fans for promoting “Hushcoin”, which some have described as “Fyre Festival for crypto.”

Cryptocons aren’t just undertaken by small groups of low-level con artists and flash in the pan social media influencers either. On February 8, 2021, “Tesla… announced that they bought 1.5 billion USD worth of BTC. The company stated that this purchase was to add “more flexibility to further diversify & maximize returns” on their cash…BTC hit an all-time high & broke the 44,000 USD mark for the first time.” For a brief moment during this storm, Tesla CEO Elon Musk became the wealthiest person on Earth. So what happened? “Well, he tweeted about the rising prices of BTC and ETH, saying that their prices “do seem high.” Bitcoin price fell after that one Tweet.”

Even institutions established to try and “stabilize” the crypto-world often are playing some other angle. For instance, Tether, which is referred to as a “stablecoin” due to its stated function of tying Bitcoin to real-world dollars and thus mitigating inflation on the blockchain, was recently prosecuted in one of the biggest criminal trials in the history of crypto. As Golubia writes in the essay linked above:

“Tethers claim to be cryptocurrencies, and run on the Ethereum blockchain, but they cannot be mined or generated by others. Tethers attempt to maintain a price of $1/Tether, and for a long time Tether claimed that it maintained exactly $1 in US dollar reserves for every 1 Tether issued. Most cryptocurrency trading markets are heavily dependent on Tethers to enable transfer between cryptocurrencies and dollars…Tether’s claims to maintain a full reserve have come under significant scrutiny. Tether claimed it would subject itself to a complete audit, but then backed off.”

According to Tether’s Wikipedia page:

“In January 2015, the cryptocurrency exchange Bitfinex enabled trading of Tether on their platform. While representatives from Tether and Bitfinex say that the two are separate, the Paradise Papers leaks in November 2017 named Bitfinex officials Philip Potter and Giancarlo Devasini as responsible for setting up Tether Holdings Limited in the British Virgin Islands in 2014. A spokesperson for Bitfinex and Tether has said that the CEO of both firms is Jan Ludovicus van der Velde. According to Tether’s website, the Hong Kong-based Tether Limited is a fully owned subsidiary of Tether Holdings Limited. Bitfinex is one of the largest Bitcoin exchanges by volume in the world…

…In April 2019 New York Attorney General Letitia James filed a suit accusing Bitfinex of using Tether’s reserves to cover up a loss of $850 million. Bitfinex had been unable to obtain a normal banking relationship, according to the lawsuit, so it deposited over $1 billion with a Panamanian payment processor known as Crypto Capital Corp. The funds were allegedly co-mingled corporate and client deposits and no contract was ever signed with Crypto Capital. James alleged that in 2018 Bitfinex and Tether knew or suspected that Crypto Capital had absconded with the money, but that their investors were never informed of the loss…

“…Research by John M. Griffin and Amin Shams in 2018 suggests that trading associated with increases in the amount of tether and associated trading at the Bitfinex exchange account for about half of the price increase in bitcoin in late 2017…Reporters from Bloomberg, checking out accusations that tether pricing was manipulated on the Kraken exchange, found evidence that these prices were also manipulated…According to Tether’s website tether can be newly issued, by purchase for dollars, or redeemed by exchanges and qualified corporate customers excluding U.S.-based customers. Journalist Jon Evans states that he has not been able to find publicly verifiable examples of a purchase of newly issued tether or a redemption in the year ending August 2018.”

As Cas Plancey writes:

“This group of companies has over ten billion in assets as of writing this piece, yet no one can provide a location where you can find executives or even a receptionist… the cryptocurrency community — a community that prides itself on advocating for trustlessness and verification of facts — refuses at every turn to demand that same level of transparency from a company that’s repeatedly promised it and lied.”

Since 2008, at the same time that the Fed was doing its quantitative easing, crypto has been shilled online as a anarcho-punk rock strike against “central banking”, completely detached from current monetary “regimes.” But as we saw during the initial explosion of Kazakhstan’s ongoing unrest, which took 15% of the Bitcoin network down, cryptocurrency is still a “currency” tied to real world things. Kazakhstan is the second biggest country in the world for Bitcoin mining, so when the government rolled out Internet blackouts in response to the protests, the cryptocurrency crashed.

This isn’t even counting the centralization that takes place within various crypto markets, regardless of the degree to which various governments regulate or don’t regulate the currencies. “As of December 2013,” Golumbia writes in his book, The Politics of Bitcoin, “half of all Bitcoins were owned by approximately 927 people, with such proletarian heroes as the Winklevoss twins of Facebook infamy among them.” By 2016, over 70% of bitcoin transactions were processed through four Chinese companies. In May 2021, Beijing set off a “great mining migration” by cracking down on cryptocurrency in response to crypto mining’s negative impact on the Chinese Communist Party’s environmental goals (yes, this also set off a crash in the value of Bitcoin and other cryptocurrencies).

The rise of cryptocons highlights a wider trend in the 21st Century political economy of the United States; concentrations of capital using the nature of digital networks to manipulate the behavior of individuals or groups within the American populace in ways which are both easily predictable and beneficial to the bourgeoisie. These concentrations of capital largely take the form of the same monopolistic tech companies, hedge funds, wealth management firms etc which have so heavily invested in businesses like Thanos over the years.

Reid Hoffman, the founder of LinkedIn and a capo in the PayPal Mafia along with the more notorious Peter Thiel, refers to this kind of investing as “blitzscaling”; “the science & art of rapidly building out a company to serve a large & usually global market, with the goal of becoming the first mover at scale.”

Companies resulting from blitzscaling by monopoly capital are known as “unicorns” as they usually become massive, Too Big to Fail businesses without turning a profit for years. Some of these companies include the big names of the data-driven “gig economy” which employs millions of the same types of young people cryptocons appeal to, and which some of the same capitalists are invested in; AirBnB, Uber, Lyft, and WeWork all come up often when discussing Unicorns. There are also well known companies of Web 2.0 included in this group, such as Snap, Pintrest, and Dropbox. Some of the statistics on Unicorns are truly head-spinning, particularly in light of the “everything bubble” popping:

“New data from PitchBook exploring the performance of billion-dollar-plus VC exits confirms Wall Street’s leniency toward unprofitable tech companies. Sixty-four percent of the 100+ companies valued at more than $1 billion to complete a VC-backed IPO since 2010 were unprofitable, and in 2018, money-losing startups actually fared better on the stock exchange than money-earning businesses. Moreover, U.S. tech companies that had raised more than $20 million traded up nearly 25 percent of 2018, while the S&P 500 technology sector posted flat returns.”

There are now 1,000 unicorn startups worth $1 billion or more. Just in January of this year, “42 startups became unicorns and four became “decacorns”—the clumsy nickname given to startups worth $10 billion or more.” As the linked Bloomberg piece explains:

“In the past, companies the size of the most valuable unicorns— ByteDance, SpaceX, and Stripe—would probably have already gone public. Today entrepreneurs feel less pressure to do so, given how easy it is for them to raise the money they need from private funders. Staying private allows many companies to avoid the additional scrutiny and potential loss of control that comes with an initial public offering. Plenty of investors are eager to get in early on rapidly evolving industries such as crypto, pushing up valuations”

In the original 2013 article that coined the term “Unicorn” to describe these start-ups, Aileen Lee notes that, of the US tech firms since 2003 she observed that only 0.07% of venture-backed startups qualified. These included AirBnB, DropBox, YouTube, Facebook, LinkedIn, Twitter, Tumblr, Groupon, and Zynga. Now, “there’s a shocking amount of investment money looking for a home—$621 billion into startups of all kinds in 2021. That’s more than double the 2020 amount and exceeds the capital raised through IPOs over the same period, which itself was a record…Covid-19’s reshaping of the economy accelerated the boom. The number of unicorns had been growing steadily until the end of 2020, when the global count was 569. Then, in the next year, it almost doubled.”

If this sounds like a highly unstable and unsustainable trend, consider Special Purpose Acquisition Companies (SPACs) which have become the financial instrument of choice for investors during the Unicorn Craze. An SPAC is a “blank check company” which is formed with the specific purpose of acquiring another company. Therefore, SPACs do nothing except assemble a massive war chest of cash from multiple sources. In turn,this gives new companies a much faster route to the public market than a traditional IPO. In 2020, 204 new SPACs debuted on major exchanges, collectively raising over $70 billion.

That same year, the Financial Times reported:

“The current statistics around Spacs are startling: so far this year 133 Spacs have been floated in the US, raising $51.1bn, nearly four times last year’s volume. A further 67 are waiting in the wings, according to Spac Research.

The list of Spac managers is swelling so fast that it now includes Billy Beane, the US baseball executive depicted by Brad Pitt in the film Moneyball, and Paul Ryan, former Speaker of the US House of Representatives.

Meanwhile, the London Stock Exchange is jumping aboard, as it explores how to lure Spacs to the UK, and a fund that has jokingly been dubbed a “Spac of Spacs” has just emerged. Easterly Alternatives is raising a $100m vehicle to invest in up to 15 other Spacs. Anyone older than a college kid may well hear echoes of the last credit boom. Back then, collateralised debt obligations, backed by tranches of loans, were so hot that financiers started creating CDOs backed by tranches of CDOs, known as CDO squareds.

Before it all ended in the 2008 financial crisis, some financiers reportedly launched a CDO cubed. If a Spac cubed materialises, keep that in mind.”

The Times explains that the massive spike in SPAC investing emerged from asset managers “sitting on mountains of cash” which they can’t invest in a way that generates worthwhile profits due to the Fed maintaining low interest rates. However, as we have seen, runaway inflation since 2021 has all but ensured an earlier than expected raising of the rates, probably toward the end of 2022 rather than 2023. This becomes disconcerting when you consider that:

“In the past decade, so much money poured into private companies that it produced huge numbers of billion-dollar privately held companies, which used to be so rare that they were known as “unicorns”. Now the private equity and venture capital players behind that money, along with company executives, want to tap public markets too.”

Gregg Larkin, the founder of “Punks and Pinstripes” who claims to have “launched new ventures and changed legacy ones at Google, Bloomberg, Uber, and across the Fortune 500” writes:

“The bullshit justification for SPACs is that they enable normal Mom and Pop investors to invest in growth-stage startups that normally would only be accessible to professional, accredited investors. It also enables small, high-growth companies to raise capital from a broader market…

The real reason SPACs exist is so that the Marc Andriessens and Peter Thiels of the world can offload shitty investments onto the general public before they implode. Normally, when an investment reaches a certain size and shows signs of trouble, the best option is to sell it to a private equity investor who can turn the company around, or admit defeat and wind the company down. With SPACs, investors have a third escape hatch: dumping those dogshit companies onto the general public. Your average CNBC viewer isn’t going to pour through the regulatory filings of a growth-equity stock looking for accounting disparities between the income statement and the balance sheet. They will, however, get jealous when their neighbor doubles their money overnight and buys a Tesla.”

Such jealousy or “Fear of Missing Out” (FOMO) is something that crops up in much of the reporting I looked at before writing this post:

“The huge question behind pump-and-dump schemes is why do they work so well? Scams have been around for a while, so what attracts people to pump-and-dump schemes? The answer is that these scams operate with FOMO (fear of missing out).”

There is, in fact, an interesting intersection between FOMO, SPACs, and an event (or perhaps, pseudo-event) which we can see as perhaps the ultimate example of our extremely volatile, pump n dump, pyramidified economy: the GameStop Gambit.

The GME Squeeze

Let us briefly recount, in a way which cuts through the bullshit about a “Reddit uprising against hedge fund managers”, what happened with GameStop and the rise of “meme investing” in 2021.

Tevye’s Stockpile argues that in early 2019, the consensus on Wall Street was that GameStop “an ancient relic bleeding out in dying malls,” was on its way out. The “bear thesis” called GameStop a Blockbuster 2.0. The “bull thesis proposed” was “relatively short term: “GME wasn’t overburdened by debt or short term liabilities, and they had a big enough cash pile to make it to the next console cycle. That’s all that needed to happen to raise the share to $18 (~200% gain at the time). These launches cyclically propelled their revenue, profit, and shares to highs, and original Reddit posters made it clear that was their endgame. The first value thesis did not even mention short interest.”

“Melvin Capital, a small hedge fund with a reported seven clients and about $10 billion assets under management (AUM) had been shorting GameStop since the quarter ending March 31, 2016.” From 2016- 2020 Melvin’s short position “was successful seeing shares slide from $31.34 April 1, 2016 to $2.80 on April 3rd, 2020. Beginning in September 2020 they began a downward spiral ending with a multi-billion-dollar-losing short position unwind at the end of January 2021.”

Teyve points out that Robinhood is free partially because “user overflow is bundled & sold to High Frequency Trading (HFT) Market Makers (MMs).” These firms make money the more retail trade is conducted on Robinhood. One such firm is Citadel, which bought into Melvin Capital on January 25th, 2021 alongside Point72 (who already owned a $1bn stake of Melvin). “The intention was to bail them out, get cheap equity, and allow them to continue or unwind the short.”

Ryan Cohen, the co-founder of Chewy, grabbed a 10% stake of Gamestop in 2020, the same year he became the largest individual shareholder of Apple. “By January 11, 2021 GME replaced three board members with Ryan and two of his Chewy compatriots making up 1/3 of the GME board.” By 2021, “the biggest holders of GME are a who’s who of big sharks. In addition to BlackRock, there’s Fidelity, Vanguard, Susquehanna, State Street Corp, etc all combined to institutionally own 110% of GME’s outstanding shares.”

Thus, when r/WallStreetBets launched the “uprising” by encouraging as many people to buy shares of GameStop as possible to inflate the price in a brief timeframe, while a handful of users made a pretty penny, it was ultimately BlackRock and other massive firms which profited the most at the expense of other financial giants. As Teyve puts it, “this isn’t a “Reddit breaking the market” thing, but an engineered shuffling of money from these billionaires over here to those bigger ones over there…Big sharks eating smaller sharks with retail traders helping fund the purchase and take the blame.”

Funnily enough, now that “meme stocks” have become old news and crypto doesn’t offer as much excitement, the new Reddit business movement appears to be encouraging young people to get into SPACs. The face of this movement is Chamath Palihapitiya.

Palihapitiya initially went viral in a video where he clutched his pearls over the social media environment he significantly contributed to creating “ripping apart society.” He has shit on hedge fund managers (“Let them get wiped out. Who cares? They don’t get to summer in the Hamptons? Who cares?”) and contributed to the narrative that the GameStop squeeze was some kind of genuine populist uprising which seriously challenged the power of hedge funds (“Instead of having ‘idea dinners’ or quiet whispered conversations amongst hedge funds in the Hamptons these kids have the courage to do it transparently in a forum…There are 2.7 million people inside wallstreetbets. I think they are as important as any hedge or collection of hedge funds.”)

Charles Duhigg has referred to Palihapitiya as the “pied piper” of SPACs:

“Palihapitiya promotes the spac as an innovation that “democratizes access to high-growth companies” while “dismantling” the “traditional capital market.” But he has sometimes acknowledged a simpler allegiance. “I want the fucking money,” he told students at Stanford’s business school, in 2017. ‘I will play the goddam game, and I will win.’”

According to Duhigg, Palihapitiya’s interest in SPACs stemmed from the bad publicity accompanying the downfall of his venture capital firm Social Capital. “Among other things, he had raised some six hundred million dollars from investors for a spac, but he had never chosen a company to merge with…Palihapitiya decided that, if he put his name and his energy behind spacs, they could become more popular—a lot more…s Palihapitiya saw it, a spac enabled anyone to invest in high-risk, high-reward companies. He branded his spac project as I.P.O. 2.0, and dubbed his first investment pool I.P.O.A. The implicit promise was that soon enough he’d get to I.P.O.Z.”

Thanks to public relations such as those deployed by Palihapitiya, we are now in a $156 Billion SPAC Bubble. As Heather Perlberg elaborates:

“More and more members of the SPAC ecosystem — a matrix of hedge funders, private-equity dealmakers, bankers, lawyers and assorted promoters — see the excesses building. They point to you’ve-got-to-be-joking valuations, questionable disclosures and, most worrisome, a growing misalignment of interests…

…In 2019, 59 SPACs raised $13.6 billion. In 2020, those figures leaped to 248 and $83.3 billion. So far this year, the totals are already at 226 SPACs and almost $73 billion, with SPACs making up more than 70% of the IPO market. Along the way, prominent financial players like Apollo Global Management Inc. and KKR & Co. have lent SPACs the legitimacy they long lacked…

…Fund managers say some SPACs are betting on companies that not long ago were struggling to raise money from risk-loving private investors. It’s become a sellers’ market: some businesses are going from one SPAC to another, shopping for better terms. Bankers have a term for the play: a SPAC-off…

..The economics are…good for Wall Street banks. They collect lucrative fees for advising SPACs, providing still more incentive to keep the SPAC game going. Citigroup, for instance, has collected about $200 million in recent years for advising on various Klein SPACs…

…Sober-minded bankers foresee this end:

In 12 or 18 months, as today’s crop of SPACs approaches the end of its 24-month lifecycle, some founders will stretch for acquisitions rather than hand money back to investors. Having to lock down deals, whatever the terms, will bring an end to the days of easy money. Eventually, much of the market will be washed out.

Many SPAC buffs predict a kind of Biblical deluge, with an Ark only big enough for Wall Street A-listers. SPACs, many say, will once again fade into the background, overshadowed by IPOs or whatever shiny new thing comes along.

Gambling and the Mental Health Crisis

While Palihapitiya was being cynical when he cried crocodile tears over Facebook causing cracks in the social fabric, he was pointing to a real problem. The mechanics of Web 2.0 which have fueled the aforementioned scams and schemes in the decade of nonexistent interest rates since 2008 are causing serious damage to mental health, particularly to Millenials who came of age at the same time as the iPhone and Generation Z, the first in American history to have never known a time without the Internet.

MIT anthropologist Natascha Schull, in her book Addiction by Design, refers to a state of mind akin to hypnosis that is produced when one is deep into a gambling machine session, what she calls The Machine Zone. According to Schull, “It’s a rhythm. It’s a response to a fine-tuned feedback loop. It’s a powerful space-time distortion. You hit a button. Something happens. You hit it again. Something similar, but not exactly the same. Repeat…It’s the pleasure of the repeat, the security of the loop.”

Schull writes that many gamblers she spoke with while researching the book “supplemented an exotic, 19th-century terminology of hypnosis & magnetism with 20th century references to television watching, computer processing, and vehicle driving…You’re in a trance, you’re on autopilot.” As one gambling addict told Schull, “Everything else falls away. A sense of monetary value, time, space, even a sense of self is annihilated in the extreme form of this zone that you enter.” Another gambler named Lola describes being “almost hypnotized into being that machine. It’s like playing against yourself: You are the machine; the machine is you.”

One study found that, “Using a slot machine task that delivered occasional jackpot wins, near misses(where the reels landed adjacent to a win) were associated with higher self-reported motivations to gamble than full-miss outcomes, despite their objective equivalence as nonwins.” As Healthmatch reported, “..the greatest reward for pathological gamers may not actually come from winning itself (“liking”)…the brain releases more dopamine in the moments before a gambling result is revealed (“wanting”).” Gamblers “like” less & “want” more as time goes on.

Healthmatch:

“What this means is that the addiction to gambling becomes independent of how many positive outcomes are experienced... pathological gamblers are rewarded with dopamine simply because of the uncertainty of playing — not necessarily only when they’re winning. In the past, winning the jackpot was an all or none scenario where you had to get all the same symbols on a single line. The invention of electronic gaming machines (EGMs)…has changed this scenario to allow for more uncertainty to be incorporated into the game…

A normalization of gambling itself has coincided with the rise of a social media environment that owes its web design to the electronic gambling machine:

“In 2018, a survey conducted by the Gallup found that 69% of Americans feel that gambling is morally acceptable (this is compared to 58% in 2009)…another 2019 survey by the American Gaming Association revealed that 57% of adults in the US feel that casinos help local economies…2021 ushered in a quick recovery for the [gambling] industry & it’s expected to hit a new record $44 billion in revenue. The US also sits at the top of the list in terms of total amount lost by country ($116.9 billion) based on data collected in 2016.””

As Forbes summarized:

“Since the Supreme Court struck down a federal ban on sports betting in 2018, any state can choose to legalize it. To date, 25 states and Washington, D.C. have already done so, and many will profit from the newly legal industry.”

“Leading up to this year’s Super Bowl, 23.2 million Americans reported plans to bet $4.3 billion on the game. A record 7.6 million people said they would bet online, up 63% from the previous year. The sports betting market in the U.S. generated $1 billion in revenue in 2020″

“…recent research suggests that gambling problems may increase as sports gambling grows explosively at the same time that mobile and online technologies evolve to create seemingly unlimited types of wagering opportunities.”

“Sports bettors have higher rates of gambling problems than other gamblers (at least twice as high), and gambling problems increase with online betting. Sports bettors who use mobile devices have a higher incidence of problem gambling”

“45% of sports betting now takes place online; this is problematic because online gambling is available any time, providing more convenience & privacy. Aggressive marketing & advertising promotions make it more difficult for sports bettors who are trying to reduce their gambling”

“Young people have higher rates of gambling problems than adults; 75% of students gambled, according to data from 2018″

What we have is a proliferation since 2008 of concentrations of capital offering people get rich quick schemes disguised as innovation which not only bankrupt the individual financially, but at the neurochemical level. OnlyFans even has an essay up giving creators advice on how to “Use FOMO to their advantage”:

“When harnessed for marketing purposes, FOMO can be a powerful tool. According to a study by Broadband Choices, the average Brit will spend £22,270 due to FOMO (Fear of Missing Out). The financial implications of this are huge for anyone trying to sell anything, and that includes OnlyFans creators…OnlyFans creators can use FOMO to their advantage by harnessing feelings of exclusivity and urgency in current and potential subscribers. These strategies will improve your bottom line, but they will also, more importantly, strengthen your relationship with your fans. The best way to get the most out of OnlyFans is to make it feel like a community rather than a transaction.”

“Lehman Bros. went bankrupt,& the Great Recession dug in when they should have been establishing themselves in the workforce…as millennials hit the point in their careers where people traditionally move into higher-paying managerial roles, the pandemic hit.

In 2020, 18% of millennial renters said they planned to rent forever, up for the third consecutive year… Among millennials who do plan to buy a home, 63% have no money saved for a down payment...The share of millennials living with their parents is also significantly higher.”

Conclusion

In the environment analyzed in this post:

“Hiking rates from their decade-plus doldrums is nothing short of economic regime change. The stock market we had before isn’t coming back. It will take a year or two of the highs getting lower and the lows never bottoming before it’s all over. After that, we’ll be living in another world. In the meantime, get your bathing suits on and prepare for the washout.”